The idealized e-commerce checkout experience, a seamless digital journey where customers effortlessly input their address and payment details before anticipating product delivery, stands in stark contrast to the reality for many consumers across Africa. In numerous African markets, the act of providing digital payment information is not a routine transaction but a significant leap of faith, often necessitating a more conversational and deeply skeptical approach to the online purchasing process.

This inherent caution transforms the typical e-commerce funnel. While a consumer might click "Buy," their finger hovers far from their payment details. The immediate priority is not the transaction itself, but the establishment of trust. This often manifests as a "do-it-yourself verification system." Potential buyers frequently initiate contact, not to finalize a purchase, but to seek tangible proof of the product’s existence and the legitimacy of the company. Platforms like WhatsApp become crucial conduits for this process. Consumers may request real-time product photos, detailed delivery timelines, and even voice notes to confirm that a human, not a bot, is engaging with them. This reliance on direct, personal interaction underscores a fundamental difference in consumer behavior and expectation compared to more digitally mature markets.

A 2020 report by McKinsey & Company aptly categorized these shoppers as "cautious consumers," a term specifically applied to e-commerce participants in the Africa and Middle East region. This designation highlights a prevailing sentiment rooted in historical experiences and the unique socio-economic landscape of these continents. The report, accessible as a PDF, delves into the imperative for retailers to adapt their strategies to this distinct consumer mindset, suggesting that technological solutions alone are insufficient without addressing these underlying trust deficits.

The Rise of Conversational Commerce: Beyond a Workaround

It is a critical misstep to dismiss the widespread reliance on platforms like WhatsApp as a mere workaround for underdeveloped digital infrastructure. For consumers in many parts of Africa, a WhatsApp conversation with a vendor is not a deviation from the norm; it is the digital equivalent of looking a seller in the eye, a fundamental aspect of building rapport and confidence in a transaction. This form of interaction fulfills a deep-seated need for personal assurance that a purely automated checkout cannot satisfy.

The complexities of building trust in digital payments were starkly illustrated by the January 2026 partnership between PayPal and Paga, a prominent mobile payment platform in Nigeria. For two decades, Nigerians had faced restrictions on receiving international funds directly into their local wallets. The eagerly anticipated agreement, allowing for the transfer of funds from PayPal to Paga wallets, was met with a deluge of skepticism and outright criticism on Nigerian social media platforms, particularly X (formerly Twitter). Freelancers and digital entrepreneurs, many of whom have experienced the frustration of frozen PayPal funds in the past, voiced their concerns, citing a "long memory of frozen PayPal funds." This collective historical experience has created a significant psychological barrier, posing a substantial challenge for the PayPal-Paga partnership to overcome, despite its potential to unlock new avenues for international commerce. The immediate reaction suggests that the legacy of past payment platform issues continues to weigh heavily on consumer sentiment, necessitating more than just a technical integration.

The Cornerstone of E-commerce: Rebuilding Trust Through Familiar Systems

The success of local payment innovators like Flutterwave and Stripe-owned Paystack in African markets is largely attributable to their profound understanding of consumers’ historical experiences with money, including the memories of restrictions and failed transactions. Their payment infrastructures are not abstract technological constructs; they are meticulously designed to mirror how people actually move capital in their daily lives. This deep integration with local financial habits is the bedrock upon which they have built their businesses.

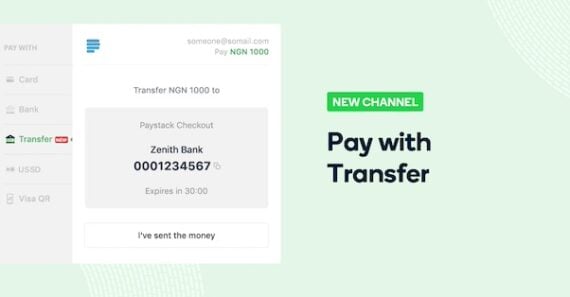

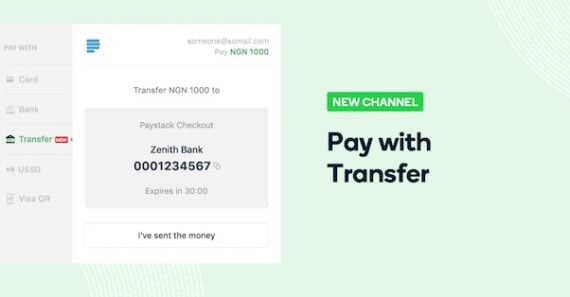

Bank Transfers: The Backbone of Nigerian E-commerce

In Nigeria, for instance, the operational reality for merchants hinges on swift access to funds. The need for settlement within one day of a transaction is paramount to maintaining business continuity and managing cash flow. Local payment solutions that facilitate this rapid transfer are therefore highly valued. From a consumer perspective, a bank transfer offers a sense of finality and verifiability. Once the funds have left their account and reached the merchant’s, the transaction is largely considered complete and auditable, providing a tangible sense of security that can be absent in other digital payment methods. This preference for direct, traceable transfers highlights a preference for transparency and control over their finances.

Mobile Money and the Power of M-Pesa in Kenya

Kenya, a pioneer in mobile money adoption, offers another compelling case study. The widespread use of M-Pesa, a mobile money service, has revolutionized financial inclusion and commerce. A key feature enabling this success is the STK Push (SIM Toolkit) protocol. This consumer-controlled security protocol allows for seamless and secure money transfers directly on mobile devices, requiring explicit user authorization for each transaction. Given that Africa accounts for approximately 70% of global mobile money payments, understanding and integrating with such protocols is not merely an option but a critical imperative for any e-commerce player seeking to succeed on the continent. Ignoring the nuances of STK Push, for example, can prove to be a costly oversight, alienating a significant portion of the potential customer base. The ubiquity of mobile phones as primary computing and financial devices in many African nations underscores the importance of these payment methods.

The Enduring Relevance of Cash-at-Kiosk Models

In markets like Egypt, the demand for physical confirmation before payment remains a significant factor. This preference underscores a persistent reliance on tangible proof of transaction and product, even in an increasingly digital world. Fawry, a leading Egyptian e-payment network, has effectively capitalized on this by offering a cash-at-kiosk model. This innovative solution allows shoppers to conveniently place their orders online but defer payment to one of Fawry’s extensive network of thousands of physical kiosks located across the country. This hybrid approach bridges the gap between online convenience and the consumer’s need for physical interaction and reassurance, demonstrating that digital innovation must often be layered upon familiar, traditional methods. The success of such models highlights that e-commerce adoption is not a monolithic phenomenon but a mosaic of diverse consumer preferences and evolving technological integrations.

The Path to E-commerce Success in Africa: Embracing, Not Eliminating, Friction

The evidence strongly suggests that foreign e-commerce merchants cannot simply import Western models and expect them to thrive in Africa through technological prowess alone. Genuine success hinges on a willingness to understand and adapt to the unique consumer behaviors and trust-building mechanisms that are prevalent across the continent. Instead of viewing the need for conversational commerce, personal verification, and familiar payment methods as obstacles to be overcome, businesses must learn to embrace this "friction" as an integral part of the customer journey.

This requires a strategic shift in perspective. E-commerce platforms and retailers must invest in building robust customer support channels, particularly those that facilitate real-time communication like WhatsApp. They need to integrate payment solutions that are not only technologically sound but also culturally resonant and historically validated within their target markets. This might involve partnering with established mobile money providers, offering cash-on-delivery options where appropriate, or developing hybrid online-offline payment systems.

Furthermore, transparency and consistent communication are key. Businesses that are open about their operations, provide clear and verifiable product information, and offer responsive customer service will be better positioned to build the trust necessary for sustained growth. The story of PayPal and Paga serves as a potent reminder that past experiences and established perceptions of financial institutions can cast long shadows, demanding patient and empathetic engagement from new entrants.

The broader implications of this approach extend beyond individual transactions. By aligning with consumer preferences and building trust, e-commerce companies can foster greater digital inclusion, empower local economies, and unlock the vast, largely untapped potential of the African consumer market. The future of e-commerce in Africa lies not in forcing a Westernized, frictionless model, but in co-creating a digital marketplace that is both innovative and deeply attuned to the needs and expectations of its users. This will involve a continuous process of learning, adaptation, and a genuine commitment to understanding the human element at the heart of every transaction. The journey may be more nuanced, but the rewards of building a truly inclusive and trusted digital economy are immense.