The journey from a simple click of "Buy" to a confirmed online purchase in Africa is far from the frictionless, linear path common in Western e-commerce. Instead, it’s a landscape shaped by a deep-seated need for trust, a preference for human interaction, and a reliance on communication channels that go far beyond a standard digital cart. This "DIY verification system," as described by some observers, is not a workaround but a fundamental aspect of how consumers in the continent approach online transactions, a reality that international and local businesses must understand to succeed.

McKinsey & Company’s 2020 report, "How Middle East and Africa retailers can accelerate e-commerce," identified this distinct consumer behavior, categorizing shoppers in these regions as "cautious consumers." This caution stems from a complex interplay of historical experiences with financial systems, varying levels of digital literacy, and a cultural emphasis on personal assurance. Unlike markets where digital payment details are readily shared, African consumers often require tangible proof of product authenticity and company legitimacy before committing financially. This manifests in real-time product photos shared via messaging apps, detailed delivery timelines, and even requests for voice notes to confirm the presence of a human operator behind the transaction.

The Rise of Conversational Commerce

This reliance on platforms like WhatsApp is not merely a substitute for traditional checkout but a vital component of the e-commerce experience in Africa. For many consumers, a chat on WhatsApp is the digital equivalent of looking a seller in the eye, building a rapport, and establishing a level of trust that is crucial for a successful transaction. This conversational approach, often termed "conversational commerce," allows for immediate clarification of doubts, negotiation, and the building of a personal connection that can overcome skepticism.

A significant event highlighting the complexities of digital payments and consumer trust in Africa occurred in January 2026 with the partnership between PayPal and Paga, a prominent Nigerian mobile payment platform. This collaboration promised to unlock a long-awaited capability for Nigerians: the ability to receive international funds directly into their Paga wallets after more than two decades of restrictions on such transfers. While heralded as a major step forward, the reception among Nigerian freelancers and the broader online community was far from enthusiastic. Social media platforms, particularly X (formerly Twitter), were flooded with expressions of vitriol and deep-seated skepticism. This reaction was not a rejection of Paga or PayPal in isolation, but a reflection of a collective, often painful, memory of past experiences with frozen PayPal funds and perceived unreliability in international financial dealings. This historical context creates a significant psychological barrier that the new partnership faces, underscoring that technological integration alone is insufficient without addressing deeply ingrained consumer anxieties.

The Bedrock of Trust: How Local Platforms Excel

The success of local payment platforms such as Flutterwave and Stripe-owned Paystack in Africa is largely attributed to their profound understanding of these consumer memories and their ability to build payment infrastructure that mirrors how people actually move capital. These platforms have not attempted to force Westernized checkout models onto African consumers; instead, they have adapted to the existing financial behaviors and trust mechanisms.

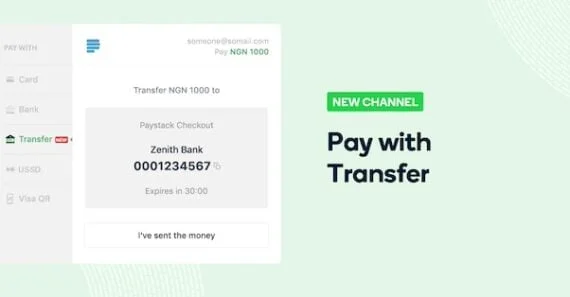

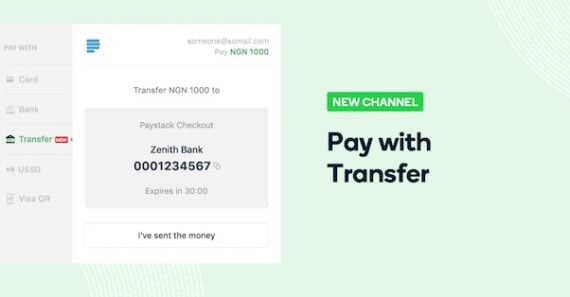

Bank Transfers: A Verifiable Transaction

In Nigeria, for instance, the immediacy of business operations necessitates rapid capital flow. Merchants require funds to settle within one day of a transaction to maintain their inventory and operational continuity. For the customer, bank transfers offer a sense of finality and verifiability. Once initiated, the transfer is a concrete movement of money, providing a tangible record that builds confidence. This is a stark contrast to digital payment methods that might feel abstract or susceptible to technical glitches or fraud. Paystack’s integration of instant bank transfers, which settle transactions within a day, directly addresses this need, offering both merchants and consumers a swift and reliable method of exchange.

Mobile Money Dominance: The M-Pesa Revolution

In Kenya and across much of East Africa, mobile money has become the dominant force in financial transactions. Platforms like M-Pesa, launched by Safaricom, have fundamentally reshaped how people access financial services. The integration of STK Push (Service Transaction Communication Protocol) technology is particularly crucial. STK Push is a consumer-controlled security protocol that enables direct money transfers on mobile devices, giving users a high degree of control and immediate feedback on their transactions. Africa accounts for approximately 70% of global mobile money payments, a statistic that cannot be overstated. Ignoring the nuances of technologies like STK Push is a costly oversight for any e-commerce player looking to penetrate these markets. The ubiquity of mobile phones and the established trust in mobile money platforms mean that businesses must offer these payment options to be competitive.

Cash-Based Systems: Bridging the Digital Divide

In markets like Egypt, where a significant portion of the population may still be more comfortable with tangible payment methods, physical confirmation before payment remains a key requirement for many consumers. Fawry, a leading Egyptian payment network, has capitalized on this by offering a cash-at-kiosk model. This allows shoppers to place an order online and then pay for it at one of Fawry’s extensive network of thousands of physical kiosks. This hybrid approach caters to consumers who are hesitant to share digital payment information online, providing them with a secure and familiar way to complete their purchases. It effectively bridges the gap between the convenience of online shopping and the need for physical reassurance.

The Path to Success: Embracing Friction

The success of e-commerce in Africa is not about eliminating friction but about understanding and embracing the specific types of friction that consumers require to feel secure and confident. Foreign e-commerce merchants cannot simply import Western digital strategies and expect them to succeed. The data clearly indicates that an approach rooted in local realities, cultural nuances, and established trust mechanisms is paramount.

The implications of this are far-reaching. Businesses that invest in understanding these unique consumer behaviors will gain a significant competitive advantage. This includes:

- Investing in Conversational Channels: Beyond chatbots, investing in human-powered customer service via WhatsApp and other messaging apps is crucial for building trust and addressing individual customer concerns. This might involve training agents to handle inquiries with empathy and providing them with the tools to share real-time information and reassurances.

- Diversifying Payment Options: Offering a wide array of payment methods, including mobile money, bank transfers, and even cash-on-delivery or cash-at-kiosk options where feasible, is essential. This inclusivity ensures that a broader segment of the population can participate in the digital economy.

- Building Localized Trust Signals: This could involve showcasing local customer testimonials, highlighting partnerships with reputable local entities, and ensuring transparent communication about delivery and return policies. Displaying security badges and certifications can also help, but they are often secondary to the reassurance provided by human interaction and familiar payment methods.

- Understanding Historical Context: As seen with the PayPal-Paga situation, past experiences with financial institutions and digital services can leave lasting imprints on consumer behavior. Companies need to acknowledge and actively work to overcome these historical hesitations through consistent reliability and transparent practices.

- Leveraging Data for Personalization: While conversational commerce is key, data analytics can help businesses understand individual customer preferences and tailor their communication and offers accordingly. This can range from suggesting preferred payment methods to providing personalized product recommendations based on past interactions.

The African e-commerce landscape is a dynamic and evolving ecosystem. While the allure of rapid digital transformation is strong, its success is contingent on a deep appreciation for the human element and the intricate tapestry of trust that underpins consumer behavior. By leaning into the conversational, valuing tangible verification, and offering payment solutions that align with local realities, businesses can unlock the immense potential of this burgeoning market and foster genuine, sustainable growth. The future of e-commerce in Africa is not about removing friction, but about mastering it.